An Applicant's Medical Information Received: Navigating the Life Insurance Underwriting Process

Life insurance underwriting involves a careful assessment of an applicant's health information to determine the level of risk. This process, while seemingly complex, is vital for setting fair premiums and ensuring the long-term stability of the insurance system. Understanding the components of this process, including the types of information gathered, how it's assessed, and the ethical considerations involved, is crucial for underwriters.

Understanding Your Medical Information: The Big Picture

Life insurance companies need comprehensive health information to accurately assess the risk associated with insuring an individual. This assessment isn't meant to be intrusive; rather, it's a crucial step in managing risk responsibly and setting appropriate premiums. The goal is to create a fair system for everyone. How long is an applicant likely to live? That's the key question driving the process.

What Kind of Health Information Do They Need?

The specific information requested varies among insurance companies, but generally includes:

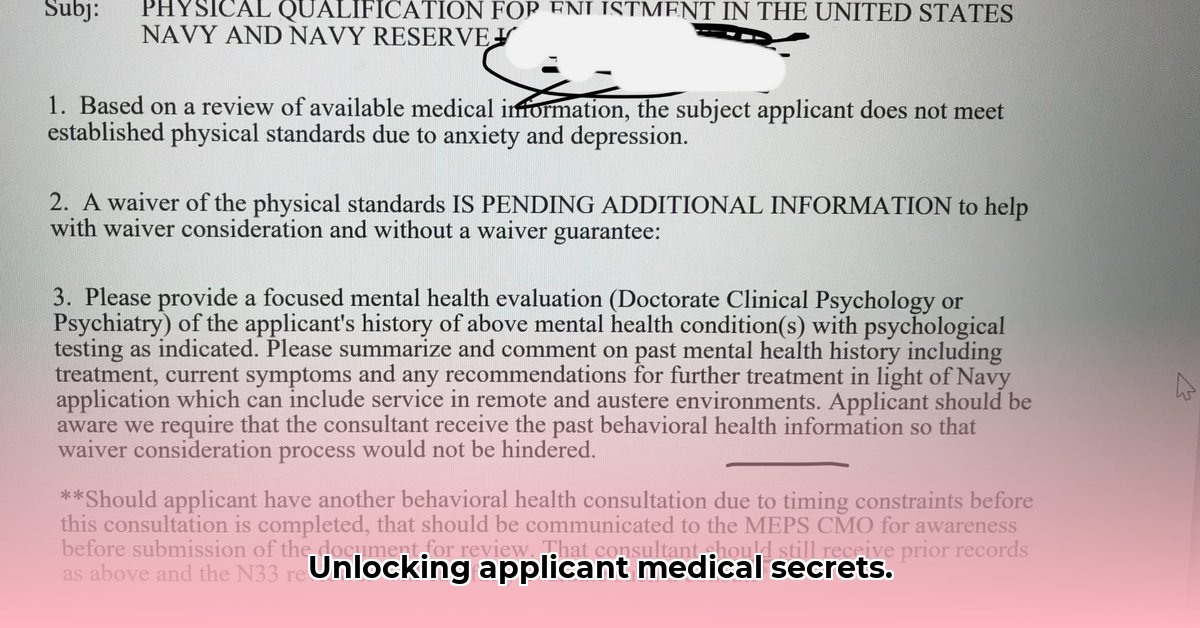

- Applicant's Health Report: A detailed questionnaire completed by the applicant, honestly disclosing their health history, including past and present illnesses, surgeries, hospitalizations, and other relevant details. This provides the applicant's perspective on their health.

- Physician's Statements: Medical records obtained directly from the applicant's doctors, offering an objective, professional view of their health status, supported by medical documentation.

- Lab Results: Blood tests, X-rays, and other diagnostic test results that offer concrete medical evidence to support the information provided in other forms.

- Prescription History: A record of medications the applicant is currently taking or has taken in the past, providing a long-term view of their health management and potential health concerns.

The combination of these sources provides a comprehensive picture, much like assembling a jigsaw puzzle where each piece contributes to the complete image.

How Underwriters Use Your Health Information: Deciphering the Puzzle

The underwriting process involves several key stages:

- Data Verification: Underwriters meticulously compare the information provided by the applicant with the information obtained from medical professionals and records. Inconsistencies trigger further investigation.

- Risk Assessment: Sophisticated tools and statistical models are used to quantify the level of risk associated with insuring the applicant, considering factors such as age, health status, family history, and lifestyle.

- Mortality Table Analysis: Actuarial tables that provide statistical information on life expectancy are used to estimate the applicant's likely lifespan.

- Policy Recommendation: Based on the risk assessment, underwriters determine the appropriate course of action: offering a standard policy, a rated policy (with higher premiums), or declining coverage altogether.

Experienced underwriters consider the full picture, integrating medical advancements and individual circumstances. It's not solely a numbers game.

Ethical and Legal Considerations: Keeping Your Information Safe

Protecting the privacy of applicant's medical information is paramount. Regulations like HIPAA (Health Insurance Portability and Accountability Act) in the U.S., and comparable regulations in other countries, establish strict guidelines for handling sensitive data. Insurance companies have a vested interest in maintaining ethical and legal compliance. Your information is treated confidentially.

Your Role in the Process: Honesty is the Best Policy

Complete and accurate information is essential. While minor discrepancies may be addressed, significant omissions or inaccuracies can lead to delays or application rejection. Transparency is crucial for a fair and efficient process.

What Happens After the Underwriters Review Your Information?

Several outcomes are possible:

- Standard Issue: A standard policy is offered with typical premiums, indicating a low-risk assessment.

- Rated Policy: A policy is offered, but with higher premiums to reflect elevated risk.

- Declined Application: In some cases, coverage may be denied if the risk is deemed exceptionally high. This is a judgment based on the objective risk assessment, not a personal judgment of the applicant.

The underwriting process aims for fairness and accuracy. However, keep in mind there can be differences in how various insurance companies handle the process. Comparing options from different providers is recommended.

How to Mitigate Underwriting Risk in Life Insurance Using AI

Key Takeaways:

- AI speeds up the underwriting process by automating data entry and document review.

- AI enhances accuracy in risk assessment through advanced data analysis.

- Careful AI implementation, with human oversight, minimizes data privacy risks and algorithmic bias. Explainable AI is crucial for transparency.

- Human underwriters remain essential for complex cases and ethical considerations.

Navigating the Medical Maze: AI's Role in Underwriting

Artificial intelligence is revolutionizing life insurance underwriting. AI can analyze vast datasets far more quickly than humans, identifying patterns and risk factors. This efficiency translates to faster processing. AI also contributes to enhanced accuracy by detecting inconsistencies or errors in the medical documentation itself.

Balancing Automation and Human Expertise

While AI offers significant advantages, it cannot replace human judgment. Algorithmic biases in the data can lead to unfair results. Human underwriters are necessary to validate AI's outputs, ensuring fairness and ethical decision-making in each case. Human expertise is vital for interpreting nuanced information that AI might miss.

Protecting Privacy: Ethics and Compliance in AI Underwriting

The use of AI in handling sensitive medical data requires stringent data security measures. Complying with regulations like HIPAA and GDPR is critical. Robust data encryption, access controls, and data anonymization are needed to protect applicant privacy. Trust is essential.

The Future of AI in Underwriting

AI's role in underwriting will likely continue to expand, leading to greater automation, improved accuracy, and potentially hyper-personalized insurance offerings. However, the responsible use of AI, with transparency and human oversight, remains paramount.